Pricing and Discount Strategies in the Spirits Sector: Analysis of the Spanish Gin and Vodka Market

TL;DR

Analysis data: evolution of average price and average discount in Spain for different gin and vodka tiers and brands, between December 2025 and February 2026, based on information from our SaaS (full details in the downloadable report).

The spirits market in Spain is undergoing a period of sustained change. The category remains closely linked to hospitality, tourism, nightlife, and home consumption—four drivers that influence both pricing and promotional activity. Added to this is a more selective consumer who compares more, seeks perceived quality, and pays attention to format, brand, and occasion.

In this context, gin and vodka continue to be two key references within the FMCG range and the digital channel. Gin maintains a solid base through tradition, versatility, and its presence in classic mixed drinks. Vodka, for its part, retains its ability to adapt to very different consumption profiles, from entry-level options to high-end propositions with strong visual and aspirational appeal.

Seasonality also plays a role. Winter, and especially December, sees a concentration of celebrations, social gatherings, and impulse buys. January and February tend to be more restrained, with lower promotional intensity and greater sensitivity to price or perceived value. Therefore, analysing what happens between December and February provides a clear understanding of how brands move once the major Christmas commercial peak ends.

For companies operating in this sector, understanding price evolution and the effectiveness of promotional campaigns is vital. It is not enough to look at general figures; it is necessary to drill down into the details by segment and region to identify growth opportunities. Below, we break down the most relevant findings obtained through our Retail Intelligence platform, focusing on the period from the end of 2025 through the first quarter of 2026.

Context: Declining Consumption and Rising Premiumisation

In 2024, spirits consumption in Spain stood at around 180 million litres, representing a fall of nearly 3.7% compared to the previous year and the second consecutive year of decline. Despite this contraction in volume, turnover remained at around 7.2 billion euros, indicating a greater contribution from the price mix and the high-end range.

This dynamic is supported by a clear trend towards premiumisation: more and more consumers are willing to pay more for higher quality cocktails and spirits, especially younger segments, who state an intention to increase their consumption of premium references. In parallel, inflationary pressure and spending restraint are driving a “drink less, but better” approach, with a growing preference for brands with perceived value, distinctive design, and higher average price points.

Price Evolution in Gin: General Stability with Growth in Trendy

The evolution of gin prices between December 2025 and February 2026 shows a relatively stable market. There is no sharp break between months, but there are clear signals regarding where growth is concentrated and where corrections appear.

If we look at price segments, the Standard range goes from €16.37 in December to €15.65 in February, representing a 4.4% drop. The Premium range barely moves, remaining practically flat (+0.1%). Ultra-Premium also remains stable, with a slight rise of 0.7%. The standout note comes from the Trendy segment, which rises from €17.69 to €18.48, an advance of 4.5%.

This breakdown says a lot about market behaviour. Gin is not experiencing a generalised price war. What is seen is a combination of restraint in the middle of the market, some pressure in the entry-level bracket, and progressive improvement in those propositions with greater brand appeal, design, or positioning.

What is happening within Standard and Premium gin

In Standard gin, the adjustment is explained by different trajectories according to the brand. Gordon’s leads the most visible fall, with a 6.9% decrease. Rives also retreats, albeit more gradually, with a 4.1% drop. In contrast, Ampersand rises by 6.5%, while Larios remains practically stable, with a variation of -0.8%.

In Premium, although the segment average barely changes, there are significant movements internally. Seagram’s rises by 16.2%, and Beefeater advances by 10.5%. Against this, Bombay barely varies and Tanqueray falls slightly by 3.2%. The result is a balance between brands pushing prices up and others acting as a brake.

Ultra-Premium and Trendy: where gin gains value

At the top end of the market, stability does not mean immobility. Brockmans concentrated the most volatility, with a peak in January of €41.88 after starting at €38.58 in December, and a subsequent correction to €38.74 in February. Other brands show more sustained evolution: Nordés rises by 5.2%, Bull Dog by 6.0% and Hendrick’s by 2.4%.

In the Trendy segment, Puerto de Indias goes from €17.90 to €18.75, with a rise of 4.7%. This is sustained growth, without large fluctuations, reinforcing the idea of consolidation. In other words, there are brands that are managing to sustain a higher price thanks to a clear product and image proposition.

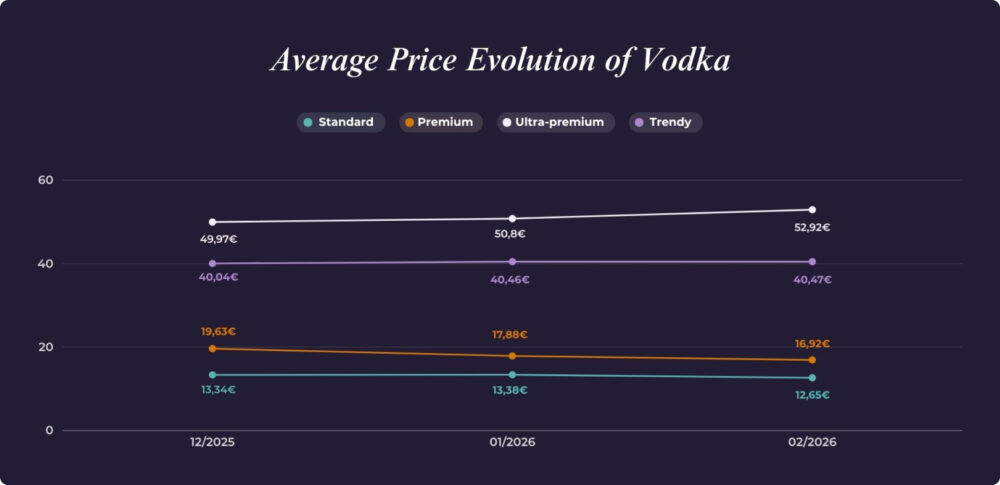

Price Evolution in Vodka: Between Weakness at Entry Level and Strength in the High-End Range

If gin conveys stability, vodka presents a more fragmented picture. Here, an evident polarisation appears between segments losing value and segments strengthening.

The Standard range goes from €13.34 in December to €12.65 in February, a 5.46% fall. The largest contraction occurs in Premium, with a 13.8% decrease. At the high end, the opposite occurs: Ultra-Premium rises by 5.9%, while Trendy remains practically flat, with a slight improvement of 1.1%.

The reading is clear: the vodka consumer is behaving very differently depending on the price bracket. The middle of the market is losing strength, while the high end manages to sustain and even raise its average price.

Standard and Premium: clear adjustment at the base and in the middle

Within Standard, opposing trajectories coexist. Smirnoff rises from €12.65 to €14.30, 13.0% more. Moskovskaya advances by 14.1% and Beveland also grows by 13.0%. However, Eristoff falls by 10.8%. This mix helps explain why the segment falls in aggregate even though several brands are rising.

In Premium, downward pressure is much more evident. Absolut goes from €17.20 to €14.57, a 15.3% drop. Skyy retreats by 15.6%. Stolichnaya, on the other hand, remains completely stable at €14.84 throughout the period. The problem for the segment is that the declines of the leading brands weigh more than the specific stability of a single reference.

Ultra-Premium and Trendy: strength at the top, calm in the visual segment

In Ultra-Premium, growth is mainly explained by Grey Goose, which rises from €55.58 to €60.01 between December and February, an 8.0% increase. Beluga remains fixed at €45.80 and Belvedere barely yields 0.7%. The result is a segment with the ability to defend price and improve its position.

In Trendy, movement is gentle. Au rises by 1.9% and Cîroc by 2.5%. These are moderate rises, closer to fine-tuning than a strong change in positioning.

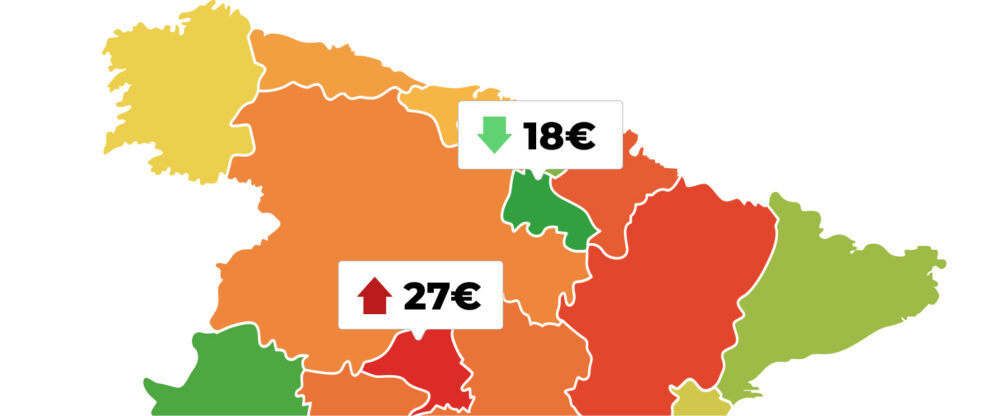

Regional Differences: Where is it Most Expensive to Drink Spirits?

Regional analysis reveals that the price of a bottle can vary significantly depending on the autonomous community. These differences respond not only to logistics but also to the density of competition and the local consumer profile.

In the standard gin category, Navarra and Madrid rank as the regions with the highest prices, exceeding €15.60 on average. Conversely, La Rioja presents the most competitive prices, with an average of €12.79. If we move to the Ultra-Premium segment, the Balearic Islands lead the maximum price ranking (€35.02), likely due to strong demand from the luxury sector and international tourism throughout the year.

In the case of vodka, Madrid stands out as the most expensive region for the Premium segment, reaching an average of €26.55, which represents a considerable difference compared to the €17.73 in La Rioja. However, in Ultra-Premium vodka, La Rioja rises to occupy the top spot on the table (€56.26) followed closely by Navarra (€55.83 average), while Galicia remains the most affordable area to purchase these high-end references.

Discount Landscape: Seasonality Rules

Promotional analysis is key to understanding how brands activate sales during off-peak periods. The data reflects a clear pattern: the Spanish market concentrates much of its promotional effort in December, leveraging the Christmas campaign (driven by gatherings, gifts, celebrations, and home restocking) as the main driver for customer acquisition. Following this, the spirits market enters a maintenance phase characterised by a notable reduction in promotional pressure.

Promotional intensity in gin

During December 2025, 68% of the analysed gin brands featured some type of discount, with an average reduction of 3.91%. However, by January and February, coverage dropped drastically to only 4 active brands.

In this scenario, Brockmans positions itself as the “agitator” brand. Its strategy does not appear to be a one-off discount, but rather constant pressure that reached -11% in December and remained at -7% in February. This suggests a tactic aimed at aggressively gaining product turnover.

Other brands use discounts more tactically. Larios and Bombay limited their promotions exclusively to the month of December to compete during the Christmas consumption peak, disappearing from promotional activity for the rest of the quarter. For their part, brands like Beefeater or Tanqueray apply what we call a “soft nudge”: small, surgical discounts, closer to a brand reminder than a true lever for price change.

The vodka promotional “blackout”

The vodka market is much more restrictive with discounts. In January and February, the category “shuts down” almost completely, with only one brand active in promotions.

Skyy leads the most extreme move in the entire report, applying a 19% discount in February. Such aggressive action usually responds to stock clearance needs or a determined attempt to displace the competition on the shelf.

It is very relevant to highlight the existence of a block of “disciplined” brands that did not apply a single cent of discount in the three months analysed. Brands like Absolut, Beluga, Belvedere, Smirnoff and Stolichnaya protect their value positioning by avoiding the promotion war, indicating a clear focus on brand consistency over specific volume.

What These Moves Mean for Spirits Brands

The combination of relative price stability, selective corrections by tier and a very seasonal use of discounts paints a scenario where the value strategy revolves around three main axes:

- Looking after mid-range positioning: declines in Standard and Premium require a clear definition of which brands will compete on price and which will be protected with lower promotional investment.

- Focusing on high-end and trendy ranges: traction in Ultra-Premium and Trendy, especially in vodka, indicates that growth is concentrated in consumers willing to pay more for distinctive attributes of quality, design and experience.

- Managing December as a “key month”: the concentration of promotions in this month reinforces the importance of properly planning offers, discounts and visibility to maximise the campaign without damaging the average price for the rest of the year.

In parallel, the rise of 70cl formats with packaging storytelling, alcohol-free variants as a tactical lever and more visual and “Instagrammable” flavours reinforce the ability of some brands to sustain and even raise prices, relying on perceived value rather than just promotions.

Beyond the Discount: How Value is Built in 2026

The spirits market in Spain is leaving behind purely transactional logic to enter territory where price is only part of the equation. The data points to something more structural: the brands that resist best—and even grow—are not necessarily the cheapest or the most promoted, but those that build a coherent proposition between product, positioning and consumption context.

This has a direct implication: competing by lowering prices outside key moments like December is not only inefficient but can erode value without generating a sustainable advantage. Instead, brands that understand when to activate the promotional lever and when to withdraw it, and that are able to justify their price through brand, design or experience, are playing in another league.The opportunity, therefore, is not in offering more discounts, but in offering them better… or in not needing them at all.