Who Leads the Digital Shelf in Anti-Ageing Cosmetics in Europe

TL;DR

Our analysis shows that leadership in the anti-ageing cosmetics Digital Shelf in Europe is local and fragmented: no single brand consistently dominates Spain, France, Italy, and the United Kingdom. This study also reveals that small improvements in digital execution can lead to major differences in visibility and competitiveness across retailers and marketplaces.

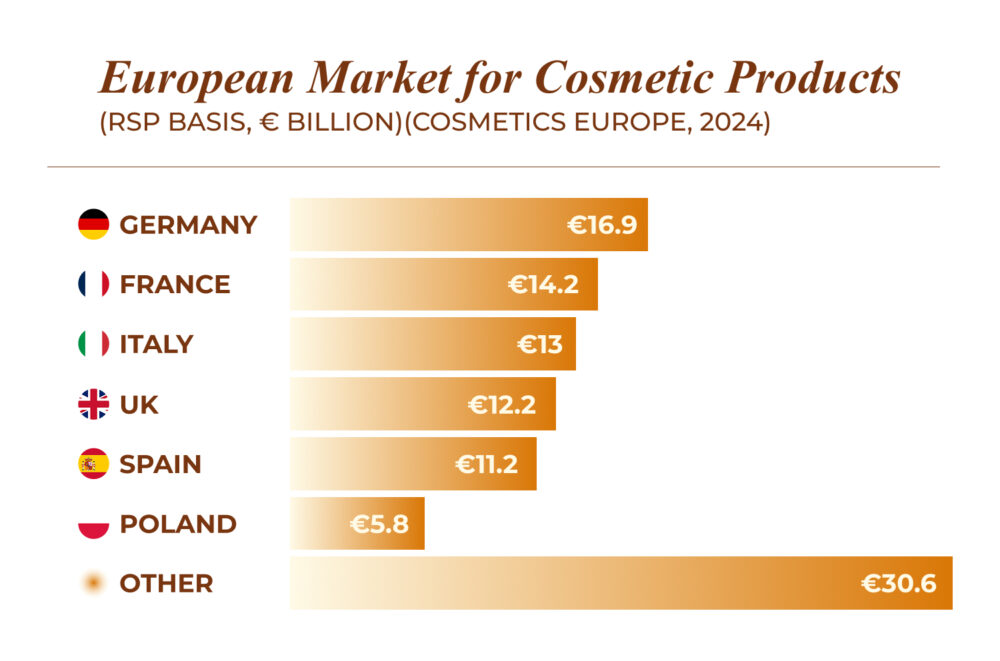

The European cosmetics market has been growing steadily for years. The sector reached €104 billion in retail sales in Europe in 2024, according to the Market Performance 2024 report by Cosmetics Europe, surpassing the symbolic €100 billion barrier for the first time and consolidating Europe as the world’s second-largest market, behind only the United States.

Source: Economic value of the cosmetics and personal care industry – Cosmetics Europe

Within this industry, the anti-ageing category is one of the most dynamic: it combines a growing structural demand, consumers with a high willingness to spend, and increasingly intense competition in both physical and digital channels.

The rise of e-commerce has profoundly transformed how cosmetic brands compete for consumer attention. Today, much of the battle for visibility is fought in the search results of platforms like Amazon, on the digital shelves of major specialist chains, and in retailers’ internal search engines. This space is known as the Digital Shelf, and monitoring it has become a strategic priority for any brand wanting to grow in Europe.

At flipflow, we have analysed the behaviour of 12 anti-ageing cosmetic brands across four markets—Spain, France, Italy, and the United Kingdom—during the first quarter of 2026, with data extracted from Amazon, Boots, Easypara, Douglas, and Primor. These are the main findings from the digital shelf visibility analysis.

What is the Visibility Index on the Digital Shelf and Why it Matters

The visibility index measures the presence and competitiveness of a brand’s products on e-commerce platforms and other digital channels. In practical terms, it reflects how often and in what position a brand’s products appear when a consumer searches for a term relevant to the category.

In the anti-ageing analysis, market-specific search terms were used: antiedad in Spain, anti-âge in France, antiage in Italy, and anti aging in the United Kingdom. The average **visibility index** stands **at around 8.3% across the four countries**, but what really stands out is the enormous dispersion between brands: some exceed 40% visibility in a specific market while others are close to 0%.

Leadership in Europe is lLocal: There is no Pan-European Champion

One of the most striking findings of the analysis is that no brand is capable of consistently dominating the four European markets analysed. Leadership is markedly local and changes from country to country.

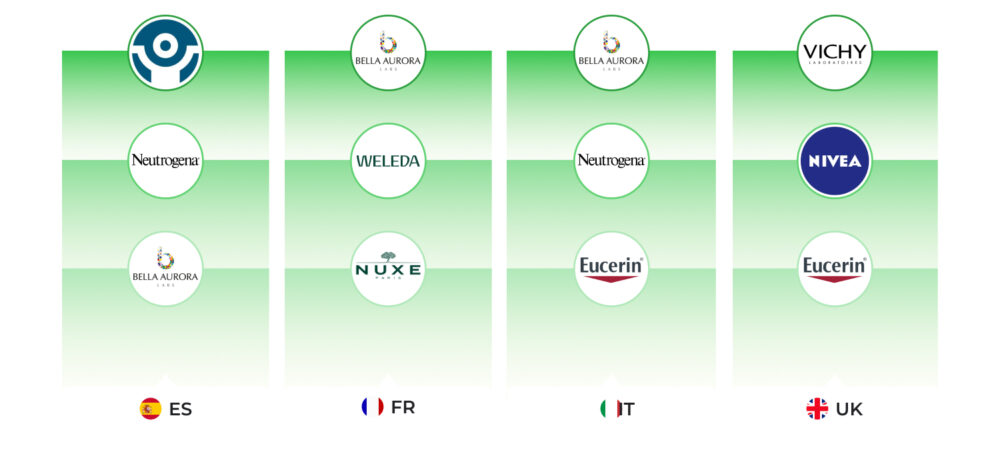

Spain: local leadership and brands with room to grow

In Spain, the average visibility index in the anti-ageing category is 8.33%. The market shows clear leadership from Cantabria Labs, which reaches 22.17% visibility and is the best-positioned brand for the search “antiedad”. Behind it is Neutrogena, with 15.79%, followed by Bella Aurora, with 12.76%. These three brands are clearly above the national average and capture a large part of the available visibility.

At the bottom are Vichy, Weleda, and Sesderma, with lower levels, which leaves room to improve presence in strategic categories and strengthen the defence of key terms.

The most interesting fact is that the Spanish market combines a very strong local leader with a solid international competitor, something that opens the door to more aggressive strategies for optimising content, assortment, and presence with retailers. For a cosmetics brand, this means that just being present isn’t enough. You have to work on the product page, keyword relevance, catalogue consistency, and availability to gain sustained positions in high-intent searches.

France: a more balanced and open market

France presents a more balanced picture. The average index is also 8.33, but leadership is more distributed: Bella Aurora leads the ranking with 17.20, followed by Weleda with 13.70 and Nuxe with 10.74.

Unlike other markets, here there is no absolute dominance by a single brand. This greater dispersion means that small operational improvements can more easily move the needle on visibility. At the bottom, Cantabria Labs and Sesderma record no visibility, while Garnier and Olay are in more modest positions.

France is, therefore, a market where digital execution carries a lot of weight. The strategic takeaway is clear: if a brand improves its positioning, optimises its content, and better manages its priority terms, it can gain presence quickly. It is one of the markets with the most room for redistributing positions. There is no absolute dominance, and that favours brands capable of optimising their presence at each retailer.

Italy: high concentration and very marked leadership

Italy is the country where concentration is most evident. The average visibility index is 8.38, but Bella Aurora reaches 37.28, a figure far superior to the rest of the competitors. Neutrogena, with 9.47, and Eucerin, with 8.01, form the chasing pack, far behind the leading brand.

This data shows a market with strong asymmetry. When a brand dominates by such a margin, others are not just competing for visibility, but for the very possibility of getting on the consumer’s radar. At the opposite extreme, Sesderma and Cantabria Labs record no visibility, showing clear space to build presence from scratch or to recover lost positions.

This scenario is particularly useful for understanding how the Digital Shelf works in highly competitive categories: if the leading brand has very fine-tuned execution, the rest need a much more consistent strategy to get close. Here, the challenge is not just to grow, but to break the barrier separating the leaders from the chasing group. Italy also proves that the Digital Shelf must be analysed market by market, because the global average can hide wide competitive differences.

United Kingdom: the most concentrated market

The United Kingdom is the most concentrated market of the four analysed. The average index remains at 8.33, but Vichy leads with 40.15, followed far behind by Nivea at 10.25 and Eucerin at 9.94.

Our reading is very clear: Vichy holds an almost hegemonic position in this market, while other brands trail far behind. The concentration around Vichy is so high that the real competitive space seems to be on the second tier, where several brands are grouped between 5% and 10% visibility. Additionally, Cantabria Labs and Bella Aurora record no visibility, and Weleda remains at a low level, confirming that the UK requires very fine-tuned execution to compete.

This environment is particularly relevant for any cosmetic brand working on digital internationalisation. The UK concentrates a lot of competitive pressure and penalises a lack of consistency in content, assortment, or positioning more than other markets. When a brand dominates here, it’s usually because its digital presence is very well built and sustained.

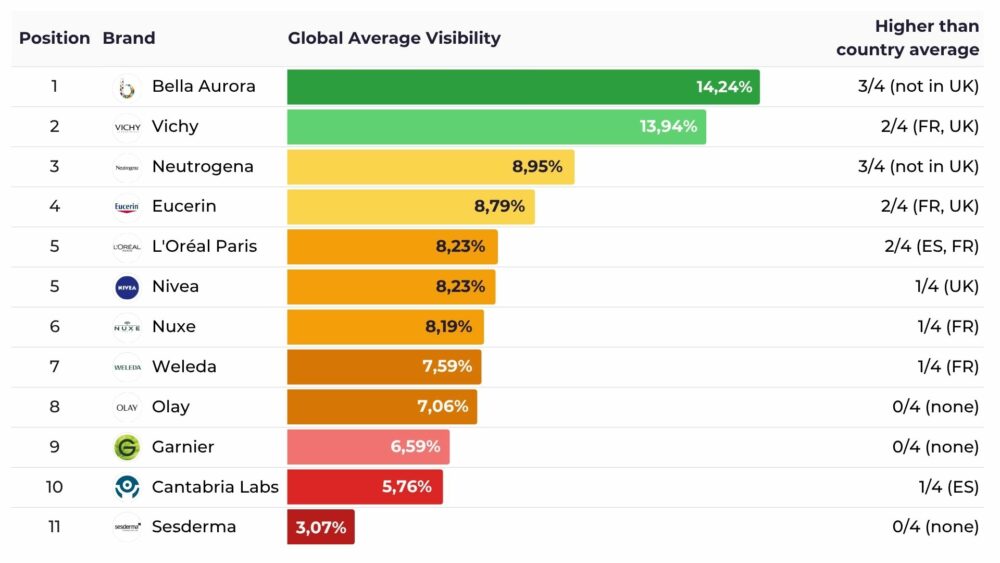

European Ranking: Bella Aurora and Vichy Lead, but with Geographical Dependence

By consolidating the results from the four countries, Bella Aurora ranks as the brand with the highest global average visibility, at 16.81%. Its position is mainly supported by Italy, where it reaches 37.28%, and France, where it leads with 17.20%. It also maintains a solid presence in Spain, at 12.76%.

However, its absence in the United Kingdom limits its consolidation as a pan-European leader. The case reflects a brand that is very strong in Southern Europe but has little to no presence in the British market within the sample analysed.

The second global position goes to Vichy, with an average visibility of 14.90%. Its result is heavily influenced by the United Kingdom, where it reaches 40.15%. In Spain, however, it drops to 4.36%. This difference shows a very marked geographical dependency.

Third place is occupied by Neutrogena, with a global average of 10.22%. The brand stands out especially in Spain, at 15.79%, and maintains a presence in all markets, although it loses strength in the UK.

Eucerin appears as one of the most consistent brands, with a global average of 8.81%. Its visibility ranges between 7.66% in Spain and 9.94% in the UK, with a volatility of just 2.28 points. This stability indicates a homogeneous execution, albeit without clear leadership in any country.

Behind them are L’Oréal Paris at 7.49%, Nivea at 7.41%, Nuxe at 7.00%, Weleda at 6.91%, Olay at 6.76%, Garnier at 5.78%, Cantabria Labs at 5.54%, and Sesderma at 2.40%.

Volatility: The Data that Reveals each Brand’s True Consistency

Average visibility helps rank the market, but volatility allows for an understanding of each brand’s consistency across countries. A brand may have a high average thanks to a single very strong market, while another may maintain a more stable presence without major peaks.

Bella Aurora shows a volatility of 37.28 points, moving from 37.28% in Italy to 0.00% in the United Kingdom. Vichy shows a similar pattern, with a difference of 35.79 points between the UK and Spain.

Cantabria Labs also reflects a strong local dependency: it reaches 22.17% in Spain but records no visibility in France, Italy, or the UK. Its volatility is 22.17 points.

At the opposite end are brands with a much more uniform presence. Olay is the most stable, with only a 1.06-point difference between its best and worst markets. Garnier also shows low dispersion, with 1.21 points, and Eucerin maintains low volatility of 2.28 points.

This reading is key for marketing, sales, and e-commerce teams. A high average visibility might seem positive, but if it depends on a single country, the competitive risk is higher. A stable, albeit more modest, presence can provide a more solid base for sustained growth.

What Cosmetic Brands can Learn from this Analysis

The anti-ageing cosmetics Digital Shelf analysis offers several useful ideas for brands selling on European digital retailers and marketplaces.

- First, leadership is local. No brand consistently dominates the four markets analysed. Spain, France, Italy, and the UK have their own dynamics, with different leaders and varying levels of concentration.

- Second, visibility can change significantly with small adjustments. In more balanced markets, like France, an improvement in content, availability, prices, reviews, or assortment can help climb rankings quickly.

- Third, consistency matters. Brands like Eucerin, Olay, or Garnier don’t always lead, but they maintain a more stable presence across countries. This regularity can be valuable for building a European strategy that is less dependent on a single market.

- Fourth, absences also speak volumes. Brands with a good position in one country may not appear in other relevant markets. Detecting these gaps allows for the prioritisation of commercial actions, review of retailer agreements, and adaptation of the catalogue strategy.

Conclusion: The European Digital Shelf is a Fragmented Territory with Real Opportunities

The anti-ageing market on the European digital shelf presents fragmented leadership, with no clear winner dominating all four markets. Each country has its own competitive dynamics, and visibility tends to concentrate on a few players per market, even though the national average is stable at around 8.3%.

For brands, this has direct implications: a good position in one country does not automatically transfer to the rest. Small differences in digital execution—catalogue quality, product page optimisation, assortment management by retailer—can translate into very wide visibility gaps on the shelf.

In such an environment, monitorising the Digital Shelf is not just a benchmarking exercise: it is a competitive lever. Brands that know their position and those of their competitors in real-time at each retailer and in each market are better placed to make quick and efficient decisions.

In the second article of this series, we will analyse the role of Retail Media (paid advertising within the retailers themselves) and which brands are buying visibility, which are winning it organically, and which are leaving spaces open to the competition.

—————————————————————————————————