Retail Media in European Cosmetics: Who Buys Visibility, and Who Earns It

TL;DR

Based on data from the first quarter of 2026 across 4 European markets (Spain, France, Italy, and the UK), we explore which anti-ageing cosmetics brands are investing most heavily in Retail Media, the extent to which they rely on this strategy to remain visible, and which are managing to build a solid presence without the need to pay.

In just a few years, Retail Media has evolved from an emerging bet into one of the pillars of the digital strategy for FMCG brands. Forecasts from WARC Media suggest that investment in this channel could reach €200 billion by 2027, consolidating a growth trend that is already transforming how brands compete for consumer attention.

Among the categories driving this investment most strongly are health and beauty, and especially facial skincare. Growing concern regarding skin ageing, prevention, sun protection, and the use of active ingredients has fuelled the rise of anti-ageing categories. At the same time, today’s consumer is much better informed: they compare prices, check reviews, analyse ingredients, and switch between perfumeries, supermarkets, marketplaces, and specialist shops before making a purchase decision.

In this scenario, gaining online visibility has become an increasingly competitive battle. For a cosmetics brand, appearing in the top search positions within Amazon, Primor, Boots, or an online pharmacy can be decisive in making it into the consumer’s basket… or falling off their radar entirely.

In the first article of this series, we analysed how organic visibility is distributed across the digital shelf in the anti-ageing category across 4 European countries. In this second analysis, we focus on the other side of that visibility: the side that is paid for.

What our Retail Media Analysis in Cosmetics Measures

The report analyses anti-ageing cosmetics brands in four European markets: Spain, France, Italy, and the United Kingdom.Our sample includes retailers such as Amazon, Primor, Douglas, Boots, and Easypara, alongside the following brands: Nivea, Eucerin, Neutrogena, Vichy, Olay, Garnier, L’Oréal Paris, Bella Aurora, Nuxe, Weleda, Cantabria Labs, and Sesderma.

It focuses on two main dimensions:

- Paid share: presence obtained through advertisements within the retailer or marketplace.

- Organic share: visibility achieved without direct investment in ads, linked to the natural positioning of the brand and its products.

The comparison between the two allows for the detection of three distinct situations:

- Brands that buy a significant portion of their visibility.

- Others that achieve good results with a solid organic base.

- Brands with an absence of paid investment in markets where their competitors are bidding.

This reading is particularly important in cosmetics, where consumers often search by need, benefit, or category rather than always for a specific brand.

The Weight of Investment

The first major conclusion of the report is that paid investment is not distributed equally across countries. Spain and the UK are the markets most concentrated in paid investment, while France and Italy present a more fragmented and accessible environment for medium-sized brands.

This means that entering and competing in Retail Media does not cost the same in every market. In the UK, advertising pressure is much more intense and the barrier to entry is higher. Conversely, in France and Italy, the competitive space is more evenly distributed, leaving more room to build a presence without the need for very high investment volumes.

In strategic terms, this necessitates segmenting investment by country. The same brand may need a strong presence in one market and a more tactical activation in another. The most common mistake would be applying the same level of advertising pressure across all countries without taking local competitor behaviour into account.

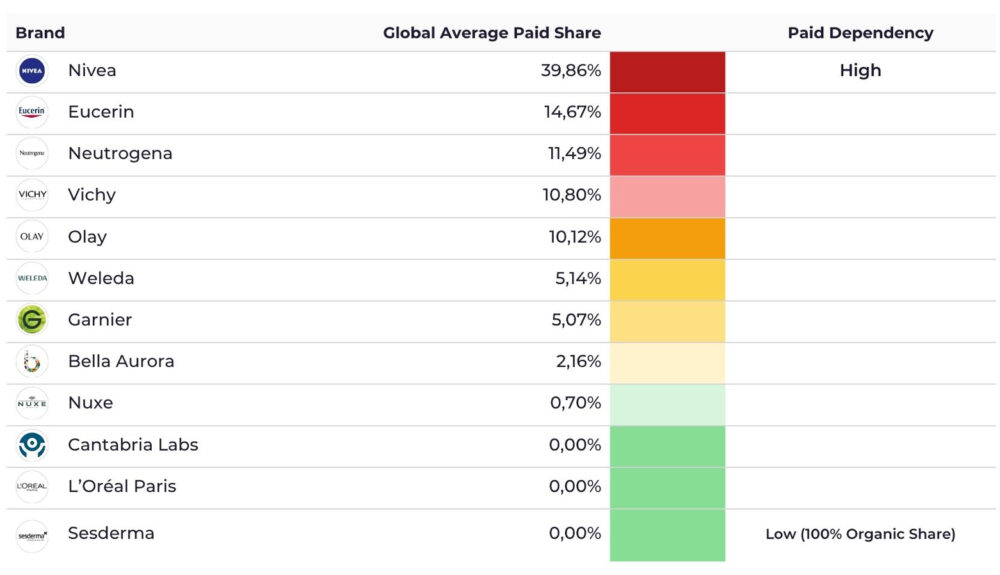

Nivea, the big spender

Nivea stands out clearly as the brand with the greatest weight in Retail Media, with a 39.86 global paid share. Its role is especially relevant because it combines scale, coverage, and sustained presence across different markets, something that allows it to defend positions in highly competitive environments.

The report also shows that Nivea adopts a flexible approach by country. In the UK, for example, it concentrates a very significant portion of its investment and reaches a strong dependency on paid visibility; in Italy, however, its profile is much more organic. This difference confirms that the strategy works based on local priorities, not a one-size-fits-all recipe for the whole of Europe.

For a cosmetics brand, this case illustrates an important idea: investing a lot is not enough on its own. Investment must respond to a specific need for defence, expansion, or demand capture. When done well, paid activity accelerates results; when done without local criteria, it only increases the cost of visibility.

Brands with a flexible mix

Eucerin, Neutrogena, Olay, and Garnier show more nuanced profiles, with different combinations of paid and organic depending on the country:

- Eucerin has a particularly high paid share in Spain and a relevant one in the UK, but is entirely organic in France. This suggests a selective strategy: the brand pushes where it needs to reinforce coverage and relies more on its natural strength where it can already stand alone.

- Neutrogena, for its part, has high levels of investment in Spain, France, and Italy, although it does not activate paid investment in the UK. Its case is interesting because it combines markets where it buys visibility intensely with others where it leaves all the weight to organic traction.

- Olay and Garnier operate with a more balanced logic between paid advertising and organic presence.

100% organic brands

At the other extreme are the brands that do not activate paid investment in any of the analysed markets. Cantabria Labs, L’Oréal Paris, and Sesderma appear with a paid share of zero across all four countries.

This does not automatically imply inefficiency. In some cases, it may reflect brand strength, good organic positioning, or a deliberate strategy not to compete in auctions. L’Oréal Paris in France is the clearest example: it achieves 100 per cent organic visibility without the need to bid.

That said, the absence of paid activity also carries a risk. In highly competitive markets, not participating in the auction can leave space for the competition to capture incremental demand, better defend certain terms, or intercept searches more easily.

Which Advertising Formats are Most Commonly Used?

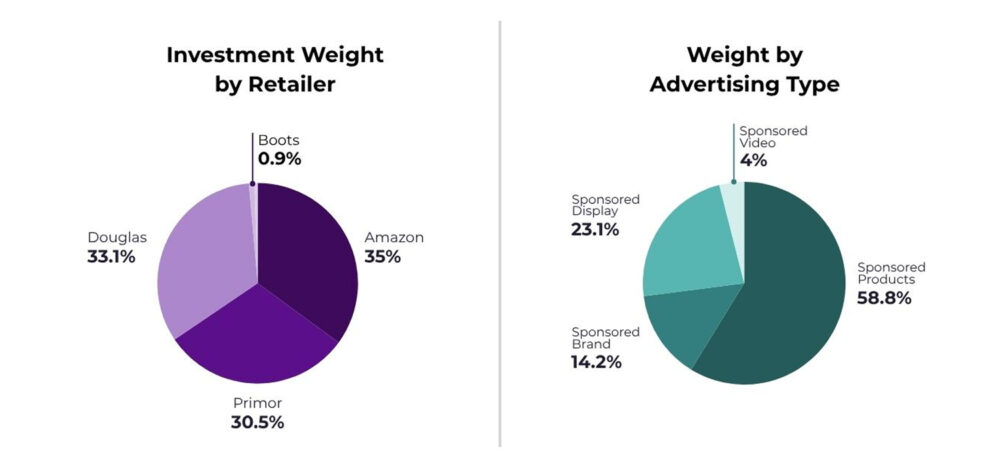

By type of advertising, sponsored products clearly dominate: representing 58.76% of all investment. This is the format most oriented towards direct conversion, appearing when a consumer is already looking for a product in a retailer’s search engine. Behind this are sponsored display (23.08%) and sponsored brands (14.20%), while sponsored video barely reaches 3.96%.

This distribution confirms that the anti-ageing category prioritises strategies for capturing existing demand over brand building or discovery. Brands invest primarily where the consumer already has purchase intent, rather than in formats that generate that intent from scratch.

Amazon, Douglas and Primor Account for Almost All of the Activation

The breakdown by retailer also offers an interesting reading. Investment is distributed primarily among three platforms: Amazon, with 35.07%; Douglas, with 33.08%; and Primor, with 30.50%.

The distance between these three channels is small. Amazon maintains a central role due to its scale and international coverage, but it does not monopolise investment. Douglas and Primor appear as highly relevant spaces for activation in cosmetics, especially in markets where they carry more weight as a shopping destination.

Boots and Easypara have a marginal weight, below 1% each in the global breakdown analysed. This suggests that, during the period studied, brands prioritised environments with higher volume, greater coverage, or higher conversion capacity.

For marketing and sales teams, this data reinforces an important idea: paid visibility in European cosmetics requires a multi-retailer strategy. Concentrating all investment in a single channel can limit reach and leave gaps available for the competition.

Paid versus Organic Visibility: The Efficiency Analysis

Beyond how much each brand invests, the relevant question is how much visibility it gets in return for that investment. This relationship between paid spend share and total visibility is what reveals whether a brand is buying its presence or earning it.

Brands with a high dependency on advertising spend

These brands are those that present the greatest strategic risk. The most extreme case is Vichy in the UK: its visibility in that market is 100% paid. In other words, without advertising investment, Vichy would practically disappear from the British digital shelf. It has 40.15% visibility in that market, but no organic base to sustain it if the budget is cut.

Nivea in the UK combines leadership and vulnerability: it concentrates 68.42% of advertising spend in that market and 32.50% of its visibility depends on payment. Its position is solid, but it is clearly sustained by budget. Neutrogena in Italy presents a similar profile of questionable efficiency: with 20% of advertising spend, 60% of its traffic depends on investment.

Brands with high organic efficiency

Brands that show the opposite pattern. L’Oréal Paris in France records a 0% paid spend share and 100% organic visibility: it is the clearest case of natural authority in the analysed set. The brand achieves presence without investing in advertising, relying on brand recognition, the quality of its catalogue, and its positioning in retailer search engines.

Olay in the UK is another standout example: with only a 5.26% paid share, it maintains an organic visibility of 95.65%. Garnier in France also presents a very efficient mix, with 84.21% organic visibility and barely 8.33% advertising spend.

Blind spots: markets where room is left for competition

The analysis also identifies a series of situations where brands with an organic presence are not activating advertising in markets where the competition is doing so. This can be interpreted as efficiency in some cases, but in others, it represents a failure to defend positions or accelerate share.

The most striking case is L’Oréal Paris in the UK: despite its brand strength, it operates with 0% advertising spend in the most competitive market in the analysis, where other brands are investing intensely.

Nuxe and Sesderma in the UK have an organic presence but no advertising investment, which limits their ability to capture additional demand or protect their search terms against competitors who are bidding.

In Spain, both Sesderma and Cantabria Labs operate entirely organically. In the case of Cantabria Labs, which leads organic visibility in that market, the absence of advertising investment could be a coherent strategic choice. However, regarding Sesderma, with low organic visibility (2.34%), the lack of paid support makes it difficult to improve its position.

Conclusion: Visibility that is Bought and Visibility that is Built

The analysis of Retail Media in the anti-ageing category leaves two clear conclusions. One is that advertising investment is highly concentrated among a small number of brands, which creates a strong asymmetry between those who can buy visibility and those who rely mainly on their organic positioning. The second is that investing more does not always mean competing better: some of the brands with the highest spend show such a high dependency on payment that any budget adjustment can directly affect their digital presence.

In this context, efficiency is not solely about increasing investment, but about building a balanced strategy between organic visibility and paid activation. The brands that achieve the best results are those that work from a solid base—with an optimised catalogue, quality content, and good positioning within retailers—and use Retail Media selectively to reinforce, defend, or accelerate that presence. When advertising acts as a complement rather than the sole driver of visibility, growth is more sustainable and dependency on spend is reduced.

In a market where Retail Media investment will continue to grow strongly in Europe, understanding which part of visibility is earned and which is bought will be key to optimising budgets, prioritising markets, and competing profitably on the digital shelf.

—————————————————————————————————