The price and format revolution in Home Care: Spanish market trends in 2025

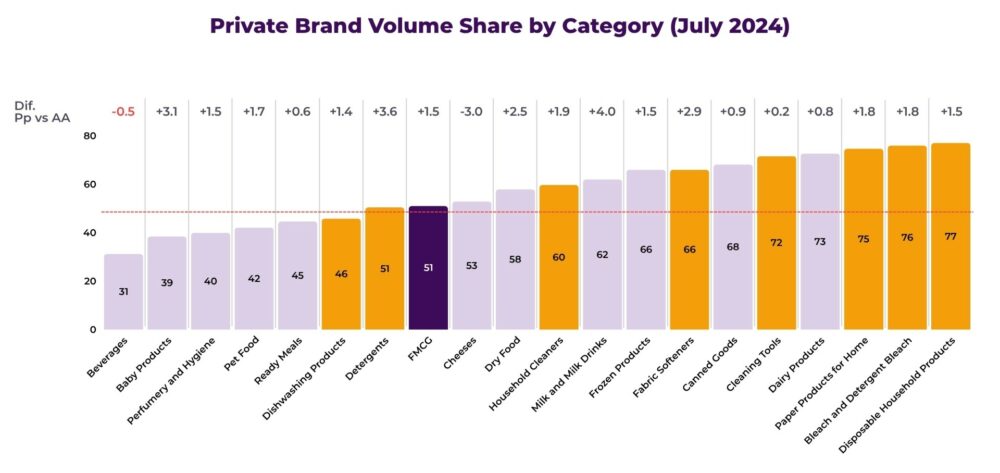

In recent months, Private Brands have gained unprecedented prominence in the Spanish market, reaching 48.5% of the total sales value in 2024. In some Home Care categories, as can be seen in the following chart, they even exceed the 70% threshold, such as “Cleaning tools” (71.7%) or “Bleach” (76.1%):

Notes: Subcategories belonging to the Home Care category are highlighted in yellow, and the FMCG sector average is in purple

Source: Study on Private Brands in Spain – Aldi – September 2024

This growing penetration is redefining the rules of the game: prices are following more complex patterns, in which the Private Brand value proposition sets the pace, while formats are evolving towards more sustainable and specialised solutions to meet an increasingly demanding market.

This analysis of several categories in the Home Care sector, carried out using our tool, delves into the strategies behind these movements and how they have shaped the sector during the final months of 2024 and the first months of 2025.

Price dynamics: Two different worlds

To understand the evolution of prices in the Home Care sector, it is essential to recognise that we are looking at two completely different commercial realities. Private Brands and Manufacturer Brands not only compete in different spaces, but they also operate with fundamentally different pricing rationales.

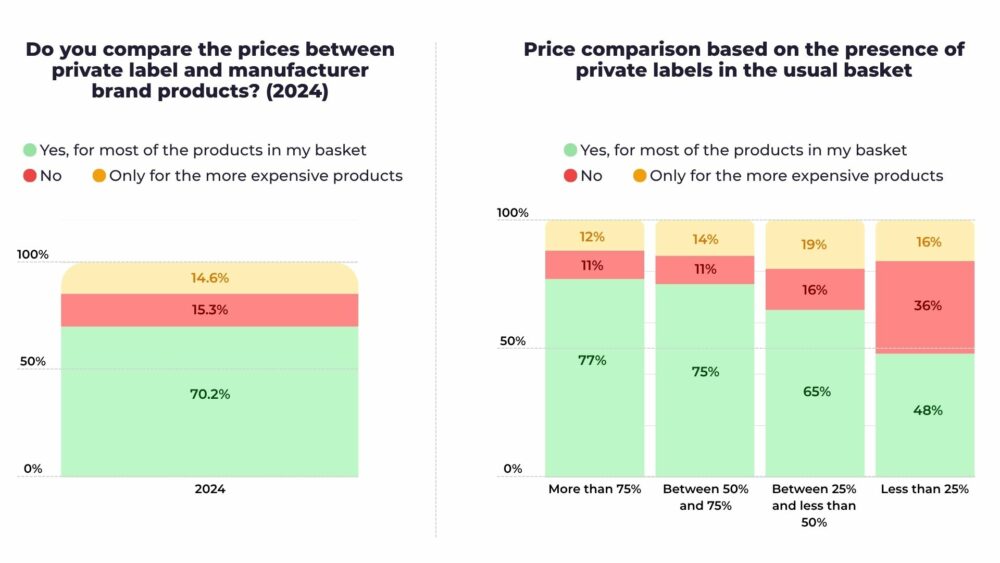

And in a country where 85% of consumers claim to compare prices between Manufacturer Brands and Private Brands, price becomes a key determining factor.

Source: Study on Private-Brands in Spain – Aldi – September 2024

Liquid Detergent: The biggest price increase for Private Brands

Liquid detergent shows the largest price increase for Private Brands of all the subcategories analysed. From December 2024 to April 2025, prices have grown by 28%, rising from 3.11 euros to 3.98 euros per unit.

This rise has not been gradual. During the first few months of the period analysed, between September and December 2024, Private Brands maintained remarkable price stability. Prices fluctuated minimally between €3.05 and €3.15, suggesting a deliberate cost-containment strategy. However, the beginning of 2025 marked an upward turning point.

Manufacturer Brands, by contrast, have maintained a completely different pricing philosophy. Their prices have moved within a high and relatively stable band, between 9.72 and 10.39 euros. The price difference between the two segments tripled in the final months of 2024, creating two clearly distinct markets.

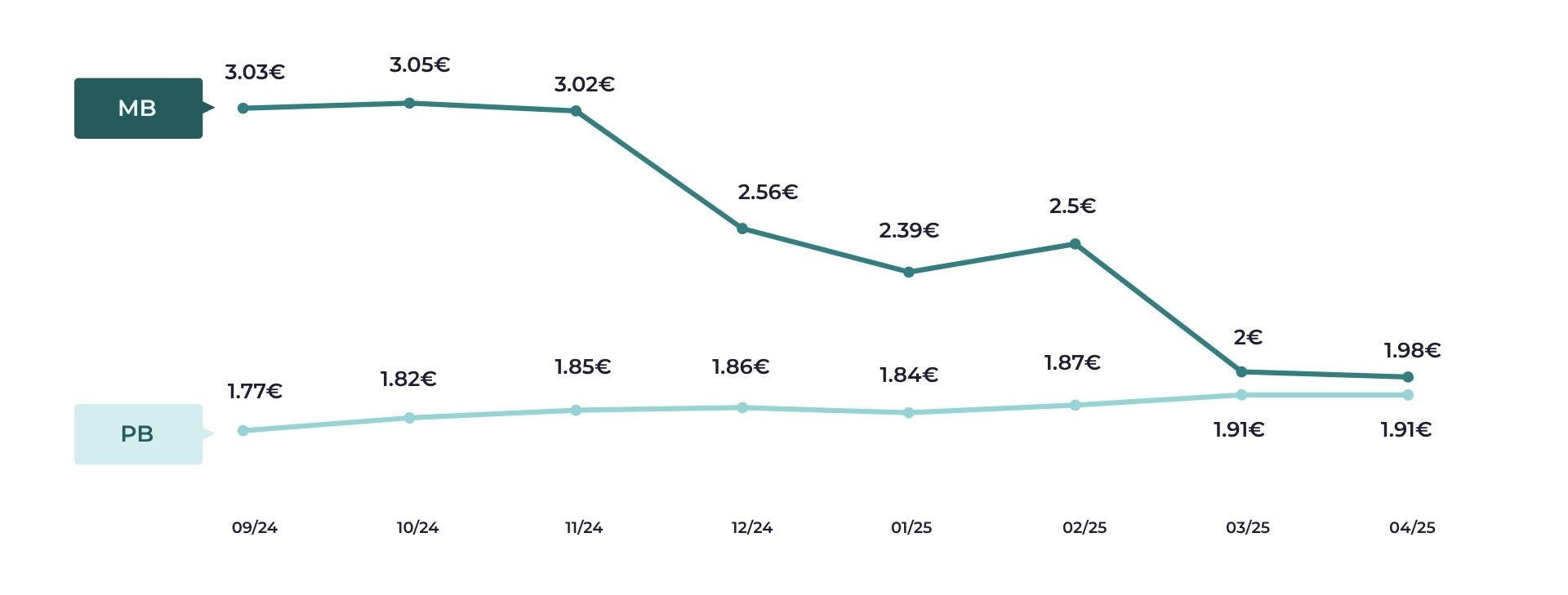

Detergent Pods: Stability versus Volatility

Detergents in a pods format perfectly illustrate the different price management philosophies between the two types of brands. Private Brands have shown remarkable consistency, maintaining prices in a narrow range between 4.30 and 4.56 euros. This stability suggests a commercial strategy focused on predictability and building consumer trust.

Manufacturer Brands have followed a completely opposite path. Their prices have experienced significant fluctuations, with sharp falls of more than two euros compared to the peaks recorded at the end of 2024. This volatility could be in response to aggressive promotional strategies or positioning adjustments in response to competitive pressure.

The partial convergence of prices at the end of the period analysed suggests that the market could be seeking a new competitive equilibrium. However, the gap remains considerable, maintaining the clear segmentation between the two types of offering.

Floor Cleaners: Consistency as a strategy

The floor cleaner market presents a particularly revealing price pattern regarding the different commercial philosophies. Private Brands have shown almost perfect consistency, maintaining practically unchanged prices at around €1.20 throughout the period analysed. This stability is no coincidence, but rather reflects a deliberate strategy of not passing cost fluctuations on to the end consumer.

This stable pricing policy for Private Brands contrasts dramatically with the behaviour of Manufacturer Brands. They have followed a downward trend for most of the period, dropping from 2.60 euros to 2.17 euros, followed by a sharp upturn to €3.01 in the last month analysed.

Dishwasher Products: Two markets, two strategies

Dishwasher products, in both gel and tablet formats, reveal pricing patterns that confirm the existence of two clearly distinct markets:

- For dishwasher gel, Private Brands have seen a significant rise of 24% between January and April 2025, going from 2.53 euros to 3.14. This evolution suggests a passing on of costs or a strategic repositioning of its price point. The price gap remains consistently wide, with Manufacturer Brands costing more than double the Private Brands in this subcategory.

- In the tablet format, Private Brands have followed a downward trend during 2025, dropping by 12% from the autumn peak. This reduction could indicate operational efficiencies or a more aggressive competitive strategy. Manufacturer Brands, remaining at prices above 8 euros, have shown less promotional elasticity.

Wipes: The unexpected convergence

The wipes market presents the most surprising case of price evolution in the entire sector. Private Brands have followed a slight upward trend, with gradual increases from 1.77 to 1.91 euros. However, the real disruptive change has come from Manufacturer Brands.

Manufacturer Brands have experienced a gradual and sustained fall since December 2024, dropping from over 3 euros to 1.98 in April 2025. This convergence towards Private Brands prices represents a fundamental change in the market’s competitive structure. The difference, which was once almost double, has shrunk to just 7 cents.

This price convergence could indicate several phenomena: a price war, the end of prolonged promotional campaigns, or a strategic repositioning of Manufacturer Brands towards more price-competitive segments.

Intensification of promotional strategies

The promotional landscape in the Home Care sector reveals a notable intensification of discounting strategies during 2025. This trend is not uniform, but rather shows specific patterns depending on the product type and its particular competitive dynamic.

The widespread increase in discounts

In all the analysed subcategories of detergent and dishwasher products, the average discount applied to products on promotion has increased in 2025. Liquid detergent perfectly illustrates this trend, with the average discount increasing by 3 percentage points, from 21.25% to 24.25% between the last four-month period of 2024 and the first of 2025. These increases suggest greater competitive pressure in the market and a growing need to incentivise sales through more attractive promotions.

In the floor cleaner and wipes categories, however, the average discount has decreased in the first four-month period of 2025. This decline may be due to less promotional pressure, an adjustment of commercial strategies in the face of more stable demand or less need to incentivise purchases in these categories.

Variations in promotional penetration

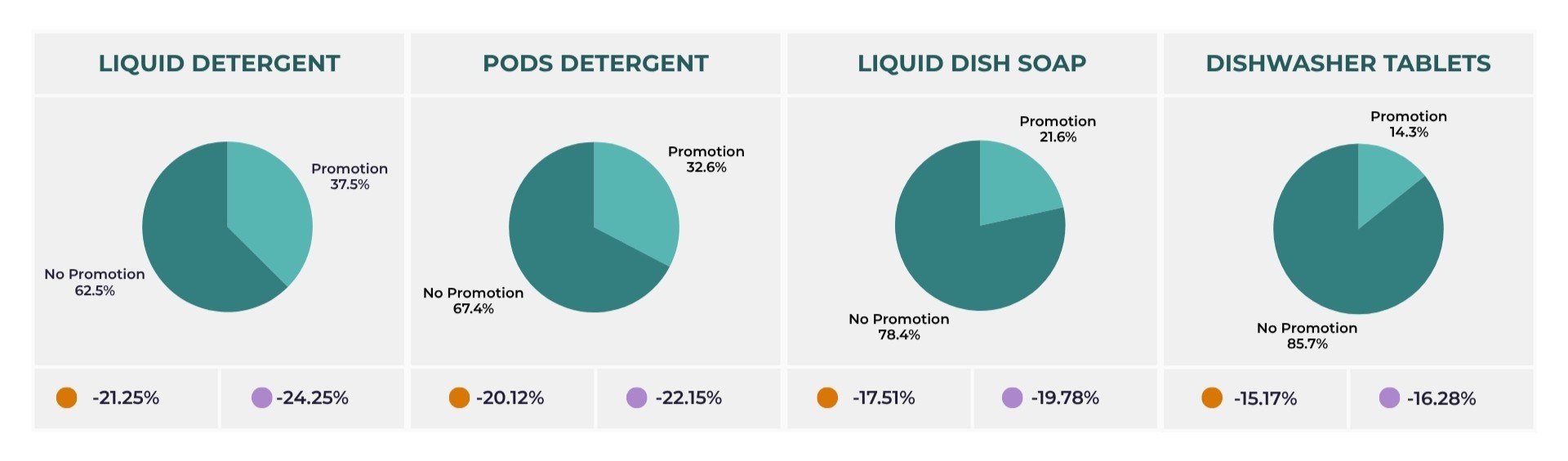

The frequency of promotions varies considerably between categories, revealing differentiated commercial strategies. Liquid detergent has the highest promotional penetration, with 37.5% of products on offer. This high promotional frequency coincides with the price increases observed for Private Brands, suggesting a compensatory strategy to maintain competitiveness.

At the other end of the scale, dishwasher tablets show the lowest promotional activity, with only 14.3% of products on offer. This lower promotional intensity could reflect a more stable market or products with lower price elasticity.

Diversity in types of promotions

Promotional strategies have evolved towards greater sophistication and diversity. Direct discounts remain predominant, but more creative formats have emerged such as ‘50% back’ or ‘70% off the 2nd unit’. This diversification allows brands to better segment their promotional strategy according to the target consumer profile.

For floor cleaners, direct discounts account for 64.41% of promotions, while for wipes they reach 56%. This preference for direct discounts suggests that consumers value transparency and simplicity in the offers for these frequently used products.

The format revolution: Sustainability and innovation

The format landscape in the Home Care sector is undergoing a fundamental transformation that goes beyond purely commercial considerations. Sustainability, convenience and functional specialisation are redefining consumer preferences and, consequently, the product strategies of brands.

Detergents: The transition towards concentration

In detergents, we observe an interesting dichotomy between the best-selling formats and innovation trends. While the liquid format in 2 to 5 litre presentations continues to dominate sales, innovation is concentrating on single-dose capsules or pods. This divergence reflects the coexistence of traditional consumers who prioritise economic value and innovative consumers who seek convenience and precise dosing.

The trend towards eco-friendly formats with compostable packaging and biodegradable formulas represents a direct response to growing environmental awareness. These formats, although still a minority in terms of volume, are gaining traction among specific consumer segments willing to pay a premium for sustainable products.

Formats in soluble strips or sheets represent the most advanced frontier of innovation in detergents. Although their penetration is still limited, they offer significant advantages in terms of reducing plastic packaging and optimising transport and storage.

Floor Cleaners: Between tradition and innovation

The floor cleaner market shows a more conservative but equally significant evolution. The traditional liquid format in 1 to 2 litre bottles maintains its dominance both in sales and in new product launches. However, the trend towards 5-litre value-size formats indicates a growing consumer sensitivity towards economic value and reducing the frequency of purchase.

Ultra-concentrated products represent an important technical innovation that allows for a reduction in packaging size without compromising the product’s effectiveness. This trend responds both to environmental considerations and to the logistical preferences of urban consumers with storage space limitations.

Dishwasher Products: The capsule format revolution

The dishwasher products segment is undergoing an accelerated technological transformation. Although traditional tablets in packs of 15 to 30 still a best-selling format, water-soluble capsules are gaining prominence both in sales and in innovation.

This type of capsule offers significant technical advantages: precise dosing, a combination of multiple functions in a single product, and the elimination of packaging waste. The trend towards phosphate-free formulas reflects both environmental regulations and consumer preferences for less harmful products.

Wipes: Sustainability and specialisation

The wipes market presents the most complex evolution towards sustainability and functional specialisation. Multi-surface wipes in a flip-top format of 20 to 30 wipes dominate both in sales and new launches, but innovation is concentrating in two main directions.

The first direction is sustainability, with the development of compostable and biodegradable wipes that respond to environmental concerns about disposable products. The second direction is functional specialisation, with antibacterial products that offer additional hygiene benefits.

Soft pack formats of 20 to 40 units are emerging as an alternative that combines convenience of use with packaging efficiency. Furthermore, they allow for greater flexibility at the point of sale and can offer cost advantages for both manufacturers and retailers.

Conclusion: A market that demands strategy, not just presence

The Spanish Home Care market is in the midst of a structural transformation that demands strategic responses from all players. The evolution of prices and formats not only reflects more sophisticated competitive dynamics, but also a consumer who increasingly values sustainability, functionality and the value-for-money ratio.

For Private Brands, the price increase in key categories such as liquid detergent or wipes indicates a move towards higher value-added territories, leaving behind their traditional role as an economical alternative. This competitive maturity poses new challenges for Manufacturer Brands, which must redouble their efforts to justify premium prices through clear differentiation —whether in performance, sustainability or convenience—, especially in categories where price convergence is more pronounced.

On the other hand, the growing complexity of promotional strategies highlights an environment where visibility and consumer incentives are becoming decisive factors. It is not about promoting more, but promoting better: segmenting, measuring and optimising without compromising the perception of value.

Formats are also in the midst of transformation: specialised and sustainable solutions are gaining prominence, which forces a rethink of product development from a more functional logic that is aligned with the values of today’s consumer. In this context, technical and format differentiation can end up outweighing price in the purchasing decision.

Ultimately, the Home Care market no longer rewards just presence or scale, but rather each brand’s ability to adapt with agility, strategic depth and truly relevant value propositions.